Why a Simple Will Might Be Costing Your Kids Their Inheritance: Testamentary Trusts for Minor Children

A testamentary trust offers stronger protection, tax benefits, and long‑term financial security for minor children compared to a simple Will. This structure helps safeguard assets, provide tax‑efficient income, support vulnerable children, and prevent lump‑sum inheritance risks through controlled distributions.

Testamentary Trusts for Minor Children: Protecting Their Inheritance

In the landscape of Australian estate planning, few tools offer as much strategic power and peace of mind as the testamentary trust. While a standard Will is a direct “handover” of assets, a testamentary trust serves as a sophisticated fortress, protecting your legacy for the people who need it most—your children.

If you are a parent of minor children, understanding how these trusts work is not just a matter of legal administration; it is about ensuring your children are financially secure, tax-protected, and shielded from life’s unpredictability.

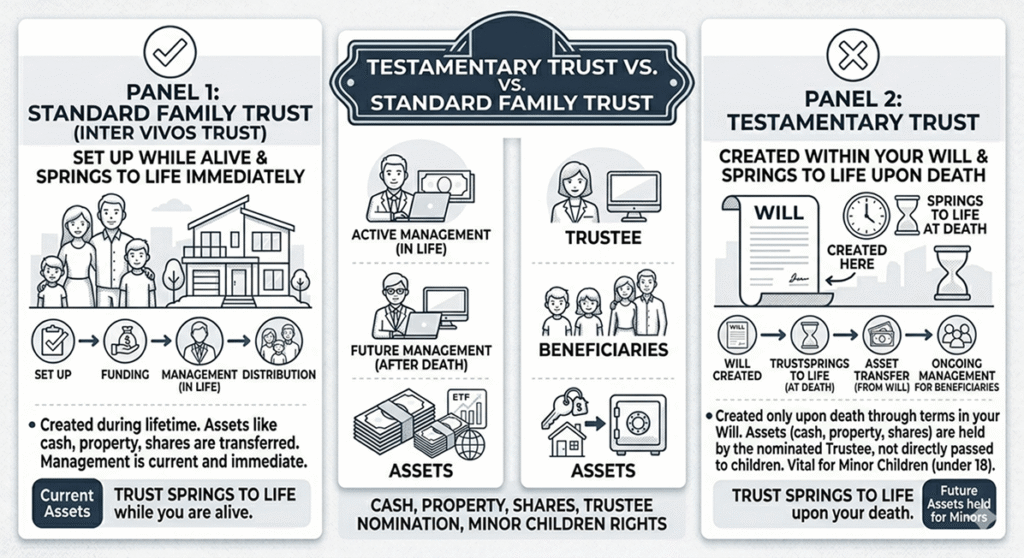

What is a Testamentary Trust?

Unlike a standard “Family Trust” (inter vivos trust) that you might set up while you are alive, a testamentary trust is created within your Will and only “springs to life” upon your death.

Instead of assets like cash, property, and shares passing directly to your children, they are held in a trust managed by a person or entity you nominate, known as the Trustee. This structure is particularly vital for minor children who, under Australian law, cannot legally own significant property or sign contracts until they turn 18.

1. The “Fortress” of Asset Protection

One of the primary reasons Australian parents opt for testamentary trusts is asset protection. In a standard Will, once an inheritance is paid out, it becomes the personal property of the beneficiary. This leaves it vulnerable to several risks:

- Creditors and Bankruptcy: If a child enters a high-risk profession later in life or faces financial hardship, assets held in a testamentary trust are generally shielded from creditors because the child does not “own” the assets – the trust does.

- Relationship Breakdowns: In the event of a future divorce or de facto separation, assets held within a well-drafted testamentary trust are often viewed differently by the Family Court. While they may be considered a “financial resource,” they are frequently protected from being part of the divisible property pool, ensuring your hard-earned wealth stays with your bloodline.

- Protection from “Spendthrift” Tendencies: We all hope our children grow up to be financially responsible, but 18 is a young age to inherit a significant sum. A trust allows you to stagger distributions – for example, giving them access to 25% at age 21, 50% at age 25, and the remainder at 30.

2. Unmatched Tax Efficiency for Minors

In Australia, the tax benefits of a testamentary trust are arguably its most famous feature. Ordinarily, if you distribute income from a regular family trust to a minor, they are hit with “penalty” tax rates (often as high as 47% for amounts over $416) to discourage people from hiding income in their children’s names.

However, the Australian Taxation Office (ATO) treats income from a testamentary trust differently. Minors who are beneficiaries of these trusts are taxed at ordinary adult marginal rates.

The practical impact is massive: As of the current tax year, a child could receive roughly $18,200 per year from the trust completely tax-free. If you have three minor children, you could potentially funnel over $54,000 of investment income into their care (school fees, medical costs, extracurriculars) without paying a cent in income tax. This “income splitting” can save families tens of thousands of dollars annually.

3. Tailored Support for Vulnerable Children

For parents of children with special needs or disabilities, a testamentary trust is an essential safety net. You can draft specific instructions to ensure the trust provides for:

- Long-term medical and therapeutic care.

- Specialised accommodation.

- Support that does not disqualify them from government benefits like the Disability Support Pension.

By appointing a professional or a trusted family member as Trustee, you ensure that the child’s lifestyle is maintained even when you are no longer there to manage the finances.

4. Avoiding the “Lump Sum” Trap

Statistics often show that large inheritances given as lump sums are frequently exhausted within just a few years. For a minor child, a sudden windfall at age 18 can be overwhelming.

A testamentary trust provides a structured financial roadmap. You can stipulate that the funds be used specifically for “advancement in life” – such as university degrees, a first home deposit, or starting a business. This ensures the capital is preserved while the income provides for their daily needs.

How to Get Started

Setting up a testamentary trust is more complex than drafting a “simple” Will. It requires specific wording to ensure it complies with Australian law and provides the maximum tax benefits.

Key considerations include:

- Choosing the Trustee: Who will manage the money? Should it be a family member, or a professional trustee to avoid family conflict?

- The Appointor: This is the most powerful role in the trust- the person who can “hire and fire” the Trustee.

- The Sunset Clause: Under most Australian state laws, trusts can last for up to 80 years, allowing you to protect wealth for your grandchildren as well.

How Growth Guardian Can Help You

FAQ

Q1: What is the purpose of a testamentary trust for minor children?

A testamentary trust protects a child’s inheritance by managing assets until they are mature enough while offering tax benefits and strong legal protection.

Q2: Are testamentary trusts tax‑effective in Australia?

Yes. Minors receive adult tax rates, which allows tax‑free income up to the standard threshold and enables significant income splitting.

Q3: Can a testamentary trust protect assets from divorce or bankruptcy?

Assets held inside a testamentary trust are generally shielded because they are legally owned by the trust, not the child.

Q4: How long can a testamentary trust last?

Most Australian trusts can remain active for up to 80 years, allowing wealth protection across multiple generations.

Date : March 17, 2026

Author : Growth Guardian